Xiaomi Surges Back to Top in Southeast Asia Smartphone Market After Four Years

Xiaomi Reclaims Top Spot in Southeast Asia’s Smartphone Market

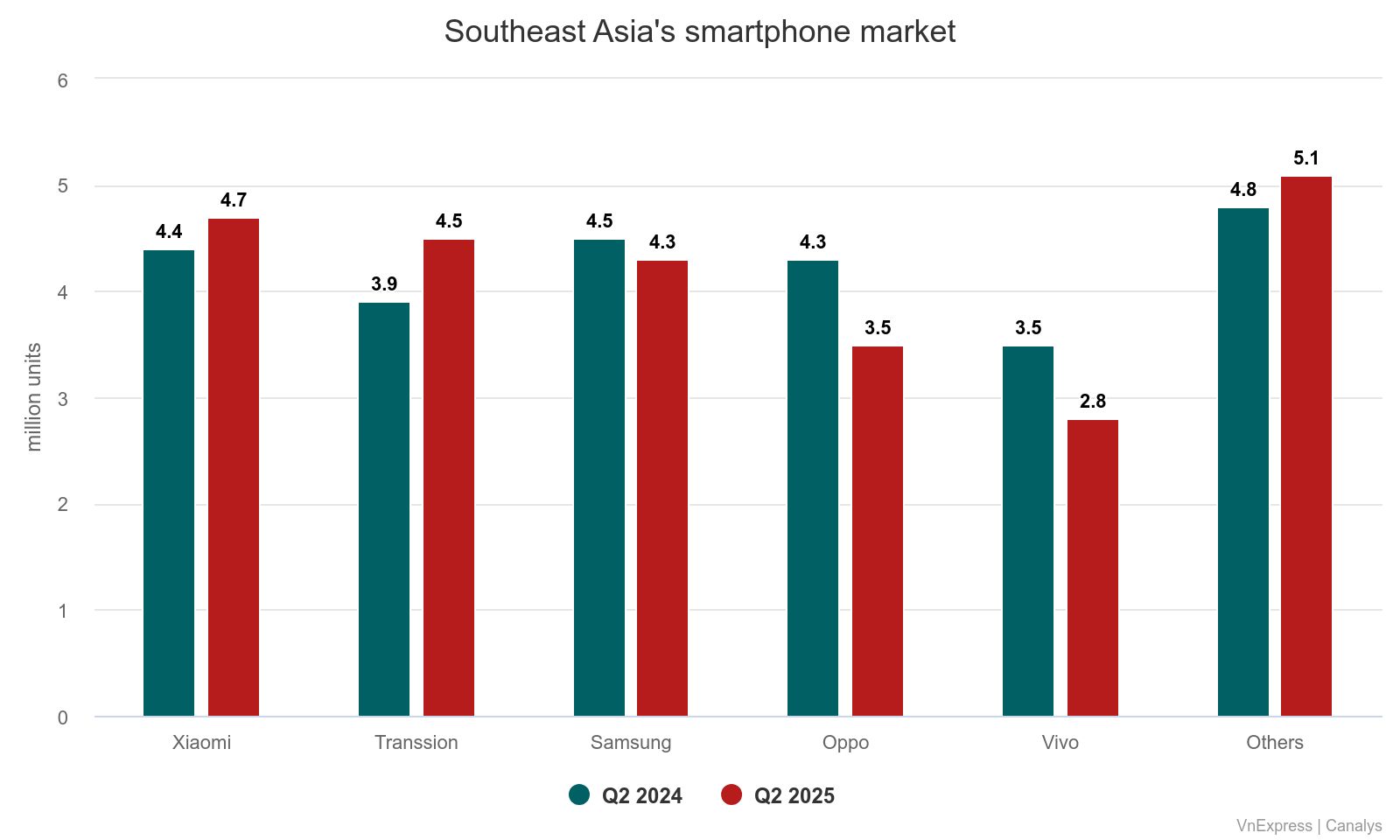

In the second quarter, Xiaomi made a strong comeback in Southeast Asia’s smartphone market, regaining the top position for the first time since 2021. The company shipped 4.7 million units, marking an 8% increase compared to the same period last year. This performance contributed to a 19% market share, driven by robust sales of its Redmi series and an expanded distribution network.

According to a report by Canalys, a U.S.-based market research firm, Xiaomi's success was supported by the expansion of its direct-to-consumer and operator channels. These efforts laid a solid foundation for scaling its sub-brands. Le Xuan Chiew, a research manager at Canalys, highlighted that shipments of Poco, Xiaomi's sub-brand, more than doubled during the quarter. Additionally, the premium Xiaomi 15 series saw a 54% year-on-year growth, signaling a shift in perception for a brand traditionally associated with budget-friendly devices.

Transsion and Samsung Maintain Strong Positions

China-based Transsion secured the second spot in the market with 4.5 million units shipped, reflecting a 17% increase from the previous year. This growth was fueled by new launches in the entry-level segment, giving Transsion a market share of 18%. Meanwhile, Samsung remained in third place with 4.3 million units, although this represented a 3% decline compared to the same period last year. Despite the drop, demand for Samsung's 5G-capable devices grew in key markets such as Vietnam and Singapore, supported by improved value propositions from models like the Galaxy A06 5G and A16 5G.

Samsung has also focused on strengthening its channel diversification and premium positioning by expanding its enterprise strategy. This approach leverages its legacy as a trusted partner for large enterprises and government sectors. According to Chiew, this strategy highlights Samsung's growing emphasis on vertical integration and business-to-business engagement, differentiating it from competitors.

Chinese Brands Continue to Compete

Two other Chinese companies rounded out the top five in the region. Oppo, excluding OnePlus, placed fourth with 3.5 million units, a 19% decrease due to intensified competition in the entry-level segment. The brand maintained a 14% market share. Vivo came in fifth with 2.8 million units, a 21% drop as the company shifted its focus toward improving profitability. It claimed an 11% market share.

Market Challenges and Outlook

Overall, the smartphone market in Southeast Asia declined by 1% year-on-year in the second quarter, reaching 25 million units. This decline was influenced by ongoing uncertainties surrounding tariffs, which continue to affect the region’s outlook.

Le Xuan Chiew noted that U.S.–China trade tensions are creating significant ripple effects, prompting vendors to realign their supply chains away from China to prioritize shipments for the U.S. This shift impacts production and stock allocation from manufacturing hubs such as China and Vietnam, disrupting inventory planning and limiting product availability.

Currency volatility, particularly a weakened U.S. dollar, is also affecting local purchasing power and retail pricing. Vendors are adjusting prices or promotions to stay competitive. Although shipment volumes remained relatively stable, looming tariff uncertainties and persistent macroeconomic challenges are dampening consumer sentiment, especially in the mass market segment.

Comments

Post a Comment